Gold Fields (GFI) is one of the most prepared gold miners to face the volatile realities now inherent in the sector, and it has taken the right steps and incorporates the right outlook, whether the price of gold falls or rises.

To that end the company has spun off some of its assets in South Africa, continued to cut all-in production costs, is targeting higher ore grade areas, lowering the size and costs of potential acquisition targets, and is looking to diversify into other commodities to spread the risk.

Price of Gold

If the price of gold rebounds in the near future, the company is prepared to take advantage of that in the weak market, which presents it with some good and inexpensive opportunities. On the other hand, if the price of gold remains below $1,300 and plummets, it is ready to cut back on projects that will no longer make economic sense.

As to the price of gold, I see the $1,300 mark as important. If gold is able to hang around that number and find support there, I think we'll see a breakout to the upper side. If it isn't able to break through and hold, I see the opposite happening, where it could plunge closer to the $1,000 per ounce to $1,100 per ounce range.

In the current environment Gold Fields has focused on shuttering marginal production projects, which resulted in attributable gold production falling from 534,000 ounces in fourth quarter of 2012 to 477,000 ounces in first quarter of 2013.

Gold Fields CEO, Nick Holland, has stated consistently that this is the direction the company will be taking in response to low gold prices. It also appears it's the strategy of the future for the company as well, as potential acquisitions are being looked at in a way that it's considered better by Gold Fields to buy smaller projects with lower production costs, than to acquire huge resources that come with higher production costs.

With that strategy in mind, I really like what Gold Fields is doing and its realistic outlook for the industry and the company. It will depend on how shareholders view the decision to lower production to better handle costs as to how it will impact the share price. Those understanding the gold market should take it as a big positive, as I believe in the near future the number of ounces mined will be far less important than the costs to mine them. With more visibility in all-in costs emerging, Gold Fields is positioned strongly to benefit from that.

So if gold prices do jump, I see Gold Fields moving up nicely from its current price level of $5.40 a share in the short term. The price of gold has jumped almost $40.00 per ounce as I write, which has brought the share price of Gold Fields up over 5 percent to $5.82 a share. With its focus on cutting costs and acquiring lower-cost projects, over the long term the miner should have no trouble returning to levels between $11.00 per share and $12.00 per share. When the price of gold takes off again, we'll see it test the $15.00 per share and $16.00 per share mark. If gold price continue to fall in the near term, Gold Fields will probably test the $4.00 per share mark, and possibly lower, depending on the depth of the drop in price.

Since Gold Fields and Nick Holland have among the more accurate understanding and outlook for the industry, I believe they'll be able to operate sustainably at these higher levels when the gold price rebounds.

My major concern is its exposure to South Africa, which has some of the highest cost mines in the world, largely because of higher wages. For example, the Western African projects include only 10 percent of labor in their costs, while in South Africa labor accounts for 40 percent of overall costs for Gold Fields, and that's about to rise.

Fortunately, it did spin off its KDC and Beatrix operations in South Africa into a separately listed company, Sibanye Gold, earlier in 2013. The company retains South Deep in South Africa, which has started to operate under a new model, which is too early to ascertain the results.

South Deep produced 63,000 ounces of the 477,000 ounces of gold produced in the first quarter by Gold Fields.

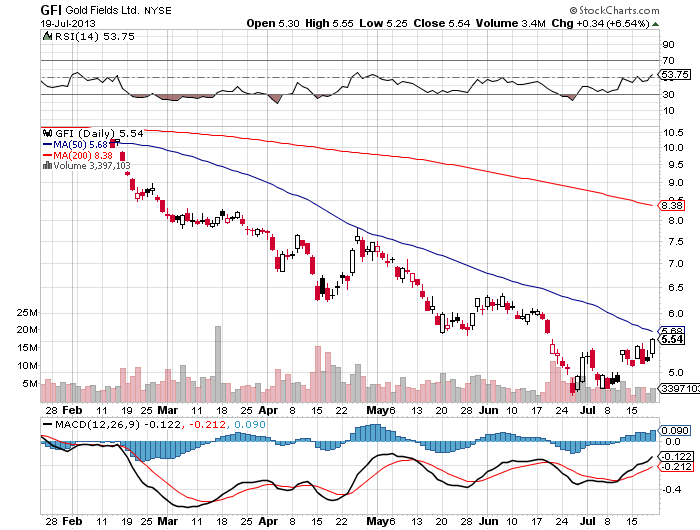

source: StockCharts

Latest Earnings Report

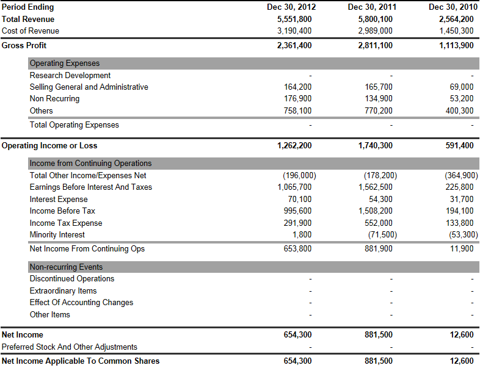

Net earnings in the first quarter came in at $27 million, down from $49 million in the first quarter of 2012, and down $41 million from the fourth quarter of 2012. A lot of that was from the spin-off of some of its South African assets, as well as the drop in gold prices and lower production. Again, a strike also affected the numbers.

None of this should be considered negative, as it's the drop in production was largely planned because the company continues to tackle high production costs. Cash costs for the quarter rose from $798 an ounce to $819 an ounce.

When taking into account what Gold Fields calls notional cash expenditure (NCE), which includes the capitalized costs for projects in its growth portfolio, and is the real cost of its gold production, it was able to lower that number by 2 percent in the first quarter from $1,355 an ounce to $1,291 an ounce. That's not insignificant, as any cost taken out of the equation is extremely important in this gold price environment. It's still a little high, but it's headed in the right direction.

Gold miners can't assume an upward move in gold will bail them out. They must continue to lower costs every way they can. I look for cutting costs first when analyzing gold miners, before production and acquisitions, as all that could do is exasperate a problem if production is increasing and each new ounce results in a loss, or at best, breaking even.

Part of the lower costs for Gold Fields in the first quarter was a reduction in capital expenditure. That's not to say the company isn't working on growing. While it is cutting back on greenfields and near-mine exploration, it's doing so to concentrate on smaller areas that have higher grades, which are less expensive to work. Greenfields expenditure was cut from $130 million in 2012 to $80 million in 2013. Near-mine expenditure was lowered from $65 million in 2012 to about $28 million in 2013.

This coincides with its acquisition strategy, which is to target smaller projects with higher ore grades and lower costs. The company is looking at projects valued at about $200 million to $250 million, although is open to as high as $500 million if it meets its existing criteria. Being a mid-tier company, it isn't looking at acquisitions in the $1 billion range.

Gold Fields will continue to keep cash in a range of $500 million to $600 million.

Source: Yahoo

Mining Strategy

We've touched a little on the mining strategy of Gold Fields, let's dig a little deeper into its plans, as all of the miners will have to incorporate a similar strategy in order to survive, let alone be profitable.

To understand gold mining in the years ahead, it must be recognized that there will be a lot lower production. Many projects that never should have been mined in the first place will be shuttered, as it will be impossible to profitably mine them. Projects will be smaller in the future, and that is part of the mining strategy of Gold Fields, according to CEO Nick Holland.

Another focus will be on higher ore grades. While this may seem obvious, it's likely a lot of the lower grade areas of a project will be abandoned unless the price of gold soars.

Holland asserts that when gold was selling as high as $1,700 an ounce, the vast majority of gold miners were just making enough to "sustain the business." Now that it's trading at under $1,300 an ounce, the overall industry is under water.

Essentially if the price doesn't go up the industry will be forced to lower production. It's as simple as that. It'll also have to target high ore areas to the expense of the rest. That was a major reason Gold Fields spun off some of its South African assets.

Wages will continue to be a major issue, and there simply isn't a lot of room for improvement there. Either workers will have to settle for increases in line with CPI, or they won't have jobs. In some parts of the world wages have been awarded as high as 5 percent over CPI year after year. It's no longer realistic, but the miners have themselves to blame for caving in over and over again. Now workers and unions have come to expect that, and the result will be an increasing number of hostile negotiations and reactions to not getting what the workers have been used to getting in past years.

Over time the expectation is there will be a lot more mechanization which would lower the number of workers. That usually happens as the companies must go deeper to get the gold. Gold Fields has already been doing some of that, although safety is part of that strategy as well. If workers and unions aren't made to understand the gravity of the situation, the gold industry as we know it in those regions will cease to exist. South Africa would probably be the first nation to fall in that regard. There's literally no more room for wages to go up there, and no amount of negotiations and strikes will change that reality. Estimates by Holland are South African gold production will probably fall by about a third within five years.

The reason why it's as difficult to make money when gold sold at $1,700 an ounce as it was when it sold for $250 an ounce is the declining ore grade. It's costing a lot more to get less gold. The distances to bring the ore to the mills also increase over time, which adds significantly to the costs; both with fuel and repairs.

This is why even if gold prices rebound some, miners will continue to be under pressure because costs are going to continue to rise for the reasons mentioned above.

If there is going to be a gold industry, that means mining higher grades, getting wage increases under control, targeting smaller projects, and slowly gravitating towards using more machines to do the work. The problem with the latter is there is a lot of R&D that must be paid for, along with proven results, before that becomes a significant cost-saving tool.

One thing the gold miners do have going for them is there is only so far the price of gold can fall before they slow production. There is no way they can continue to produce at a loss. When that happens prices will have to go up if there is real demand for physical gold. If not, we'll see a huge decline in the size of the industry, as well as the many miners in it. Gold Fields already anticipates a more lean company, although will acquire a project that has high ore grade and they can get at a good price.

Balance Sheet

(click to enlarge) Source: YCharts

Diversified Mining

When asked about growing the gold industry, Holland gave an answer that which points to what could be a big change for Gold Fields. He suggested moving away from gold in and of itself and towards a number of other resources miners could produce. Among those for Gold Fields are coal, platinum, iron ore and Ferromanganese, among others.

Holland wants to produce those commodities incrementally when the right conditions are in place. That speaks to diversification, and the fact that gold doesn't appear to be a metal that can be mined profitably on its own, or even with some byproduct.

What it appears to mean is Gold Fields isn't just going to attempt to increase byproduct, but to focus on opening up new markets it will directly compete in concerning various commodities. In other words, it's probably going to go beyond byproduct to some major production with these other opportunities.

Personally, I think this is what the gold miners must do now and over the long haul to survive and compete. I don't see gold being a commodity that can be successfully mined at a profit on its own. There will have to be significant complementary commodities to balance the portfolio of a company.

There is no doubt Gold Fields will slowly move in that direction. To me the sooner it does that the better, although the existing commodity environment will make it slow going.

Conclusion

In relationship to the mining of gold, it appears Gold Fields, as it stands today, is going to become a smaller producer of the yellow metal. As Holland has stated, even at $1,600 and $1,700, companies are just able to operate sustainably. Zeroing in on high ore grades and smaller projects will help the company compete in the years ahead, even if production falls.

This is the new reality. The amount of gold production is increasingly becoming less important, while the all-in costs is the most significant factor, along with the price of gold. Gold miners may sound impressive when reporting increases in production when compared with smaller competitors in the future, but if they're doing it at break even or a loss, it won't be long before that is exposed and shareholders suffer. I don't see that with Gold Fields, as Holland has been open about the condition of the company, costs of gold, and what must be done for the gold miner and the industry to be successful in the future.

Even though Gold Fields may retain the name 'gold' in its title, we'll surely see it starting to gravitate towards being a diversified miner. The key there is being sure to bring production on line for specific commodities when it makes financial sense. This will take some time to do, but will definitely be worth the undertaking and expense. I think the days of pure gold miners are over; meaning going beyond the byproduct and growing into competitors targeting commodities outside of the usual focus of the companies. That is the stated case with Gold Fields, and we can expect to see that in the years ahead.

As for production costs, you can see from the time when gold was selling for about $250 an ounce to today, the costs continue to rise over time, and if they continue to rise at the rates of the last 10 years, $3,000 an ounce gold may not be enough to cover expenses going forward (five to ten years from now). That may sound ridiculous, but the price of gold is over 5 times what it was back in the latter part of the 1990s, and companies today struggle to generate a profit. As long as costs rise at a much slower rate this shouldn't be a problem for Gold Fields, but it does reveal the challenge faced by it and the gold mining segment in general.

One major advantage Gold Fields has over many of its competitors is it has one of the best CEOs in Nick Holland, in my opinion. There is no fooling around or being in denial with him, but a refreshingly honest and open look at the industry in general, and Gold Fields in particular. With that in mind I see Gold Fields as a bellwether of where the gold mining sector must and will go, and it is one of my favorite gold mining companies. I will like it even better when it diversifies.

GFI just recently came off of a 52-week low, but I would like to see where the price of gold goes in relationship to $1,300 an ounce before looking for an entry point, even though where it stands now is pretty good.

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/charts/metals/gold/t24_au_en_usoz_2.gif)